Credit Score Dropped After Payment. Seeing your credit score drop after making a payment feels counterintuitive. You paid down debt—so why did your score decrease? The answer lies in how credit reporting cycles, utilization ratios, and scoring algorithms operate.

Below is a precise breakdown of the most common reasons your credit score dropped after a payment—and what to do next.

1. Your Payment Hasn’t Been Reported Yet – Credit Score Dropped After Payment

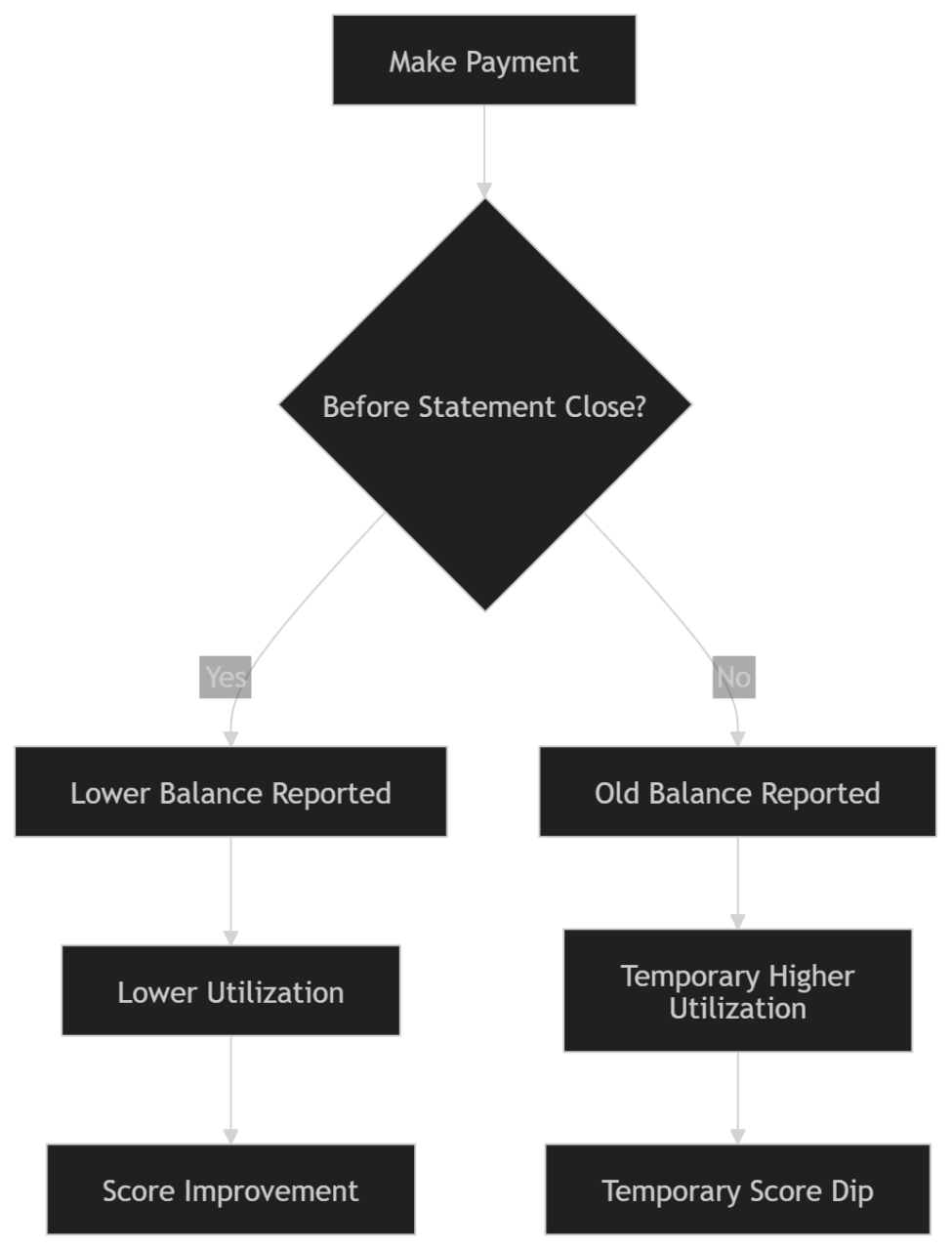

Credit card issuers typically report balances to credit bureaus once per month—often on the statement closing date, not the payment date.

If you made a payment after the statement closed:

- The higher balance may already have been reported.

- Your lower balance will not appear until the next reporting cycle.

What to Do:

Wait for the next statement cycle. Scores often rebound once the updated balance is reported.

2. Your Account Reported as “Paid Off” (Zero Balance Penalty)

Surprisingly, reporting a $0 balance on all credit cards can cause a small temporary score dip.

Scoring models prefer to see:

- Active revolving credit usage

- Very low utilization (1–5%)

When all cards report zero usage, some models interpret this as inactivity.

Fix:

Allow one card to report a small balance (1–3% utilization), then pay it off after the statement posts.

3. Credit Utilization Was Still High When Reported

Even after making a payment, if your reported balance remains above 30%, your score may still reflect elevated risk.

Example:

- $5,000 limit

- Paid from $4,500 down to $2,000

- Utilization = 40%

While improved, 40% is still high enough to suppress scoring.

Target:

- Under 30% for acceptable impact

- Under 10% for strong score gains

4. Another Account Changed Simultaneously – Credit Score Dropped After Payment

Credit scores update based on your entire profile—not one account.

Your score may have dropped because:

- Another credit card reported a higher balance

- A loan balance update shifted your credit mix

- A hard inquiry was added

- An old account aged off your report

Always review your full credit report before assuming the payment caused the drop.

5. Closed Account After Payoff

If you paid off and closed a credit card:

- Total available credit decreases

- Utilization ratio may rise

- Average account age may decline over time

This can result in a temporary or moderate drop.

Solution:

Keep older no-annual-fee cards open whenever possible.

6. Installment Loan Balance Thresholds

If you paid down a loan (auto, personal, student), crossing certain percentage thresholds can temporarily shift scoring calculations.

For example:

- Moving from 11% to 9% remaining balance may adjust scoring weight differently than expected.

Installment loan scoring works differently from revolving credit scoring.

7. Score Model Fluctuations

Different scoring models react differently to payments:

- FICO® vs. VantageScore®

- Auto loan score vs. credit card score

A drop in one model does not necessarily reflect long-term damage.

How Credit Reporting Timing Works – Credit Score Dropped After Payment

How Long Does the Drop Last?

In most cases:

- 7–30 days if due to reporting cycle

- 1–2 months if utilization remains elevated

- Longer if tied to account closure or inquiries

Temporary drops are common and often self-correct.

Immediate Steps to Stabilize Your Score

- Check your credit report for updated balances.

- Confirm the statement closing date.

- Reduce utilization below 10%.

- Avoid new credit applications.

- Keep at least one small balance reporting.

- Ensure no late payment was mistakenly recorded.

Precision monitoring prevents unnecessary concern.

When to Be Concerned

Investigate further if:

- A late payment was incorrectly reported.

- An account shows delinquent status.

- A significant drop (50+ points) occurred unexpectedly.

- Identity theft is suspected.

Dispute inaccuracies immediately with the credit bureau.

Final Insight – Credit Score Dropped After Payment

A credit score drop after a payment is usually a timing or utilization issue—not a punishment for responsible behavior. Credit scoring systems operate on reported data cycles, not real-time transactions. With proper balance management and awareness of statement dates, temporary dips can be avoided and reversed efficiently.